To view this message as a file, click here.

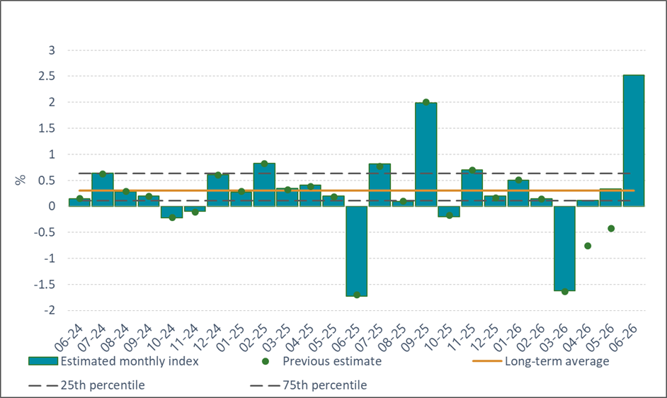

the average monthly growth estimate for the three months from April to June. As such, the rapid growth is due to the exit from the Index of the low level of activity that was experienced in March due to Operation Roaring Lion. The Index was positively impacted data on credit card purchases, goods exports, and the import of consumption goods and of manufacturing inputs in April and May, trade and services revenue data and industrial production data in April, labor market data and the retail trade index in May, and the Tel Aviv Stock Exchange General Shares Index and the Nasdaq Index in May. The local indicators available for June also show stability or some increase (Tables 1 and 2).

The pace of increase of the index is above the long-term growth trend (about 0.3 percent).

The Index for the past two months was revised upward with the completion of data that were previously missing and with the additional downward revision in growth data for the first quarter of 2026.

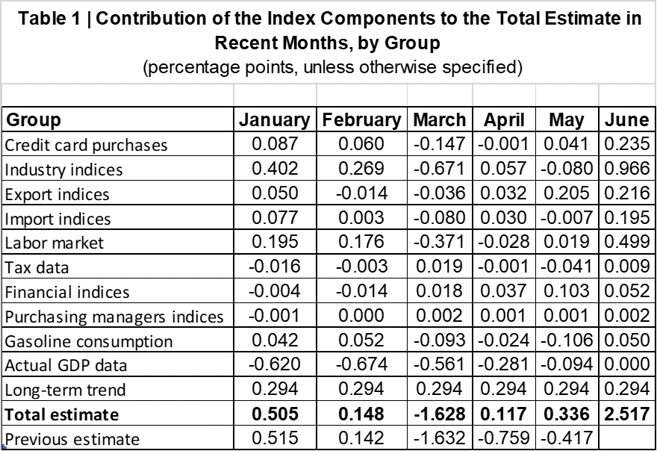

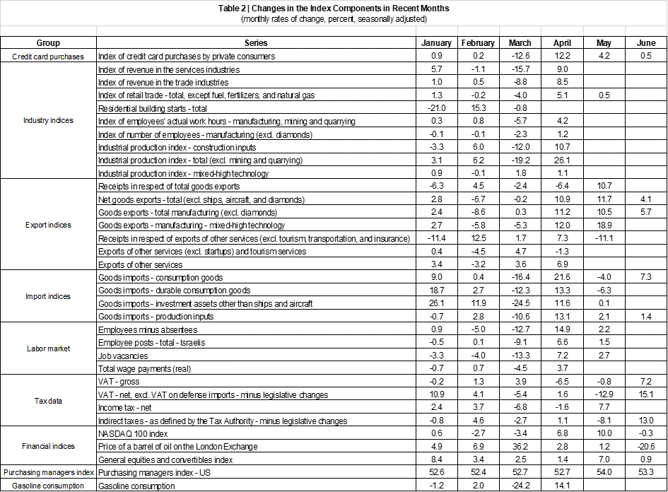

Figure 1 presents the Index data over the past two years. Table 1 presents the contributions of the Index’s components to the overall estimate and the revisions to the Index, and Table 2 presents the monthly rate of change in the Index’s components.

FIGURE 1: The Monthly Index of Economic Activity

* The table presents the contribution of each group of components in the monthly index, such that the monthly estimate constitutes the sum of the contributions of each of the components detailed in the table. Some of the raw data influence the monthly estimate with a lag or influence the estimates of several months.