1. The Exchange Rate

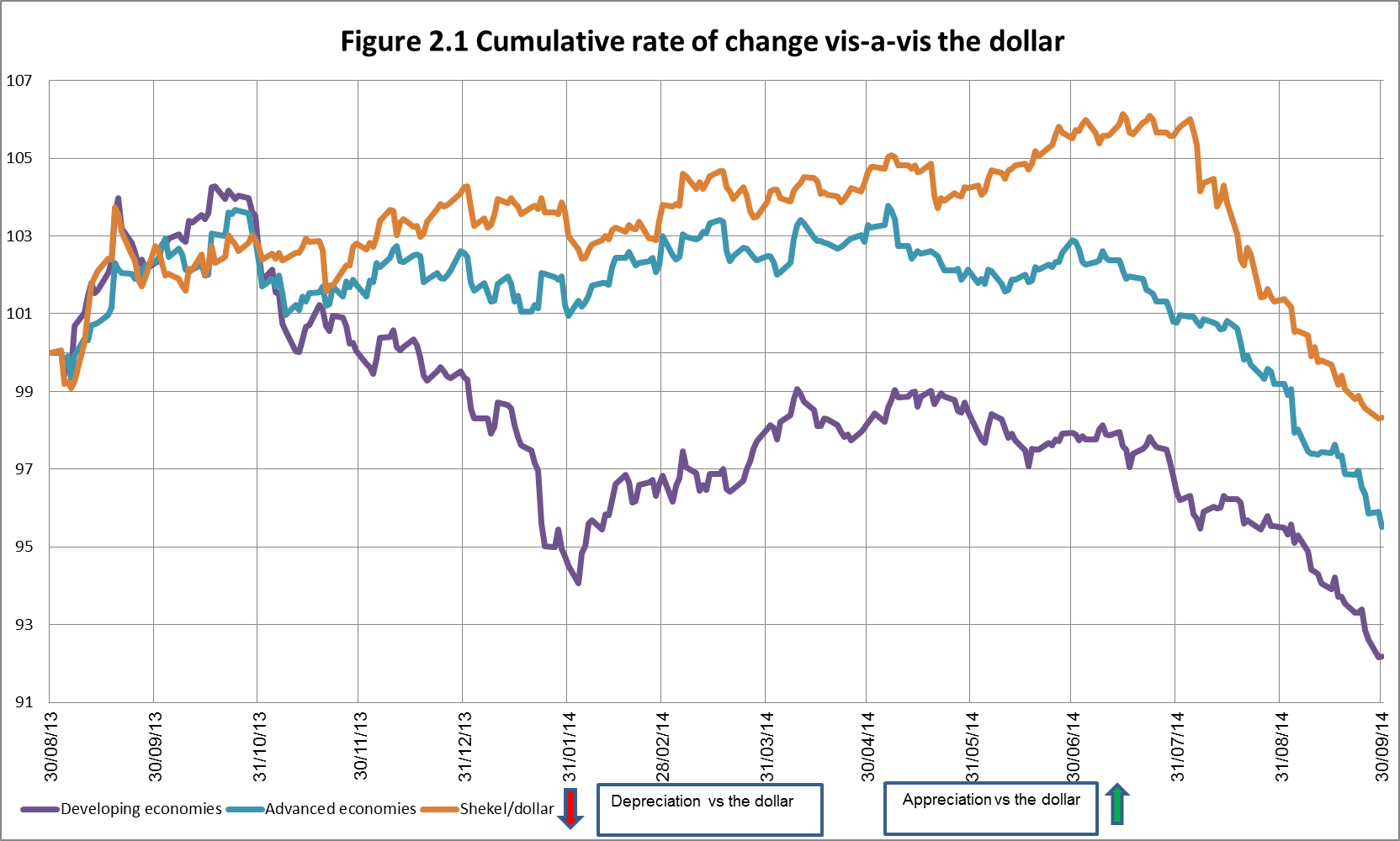

The dollar strengthened against the shekel, in parallel with strengthening of the dollar worldwide.

In September, the shekel weakened by about 3.6 percent against the dollar, and strengthened by about 1.2 percent against the euro. Thus, this month as well there was a continuation of the trend of depreciation of the shekel vis-à-vis the dollar, with a cumulative depreciation since August of 7.6 percent.

Against the currencies of Israel's main trading partners, in terms of the nominal effective exchange rate of the shekel (i.e., the trade-weighted average shekel exchange rate against those currencies), the shekel weakened by about 0.6 percent.

The depreciation in September was mostly global, as the dollar strengthened against most currencies by high rates—including by about 4.9 percent against the euro, by about 4.8 percent against the Swiss franc, by about 2.5 percent against the British pound, and by about 5.7 percent against the Japanese yen. Likewise, the dollar strengthened against the index of advanced economy currencies by about 3.85 percent (see Figure 2.1).

2. Exchange Rate Volatility

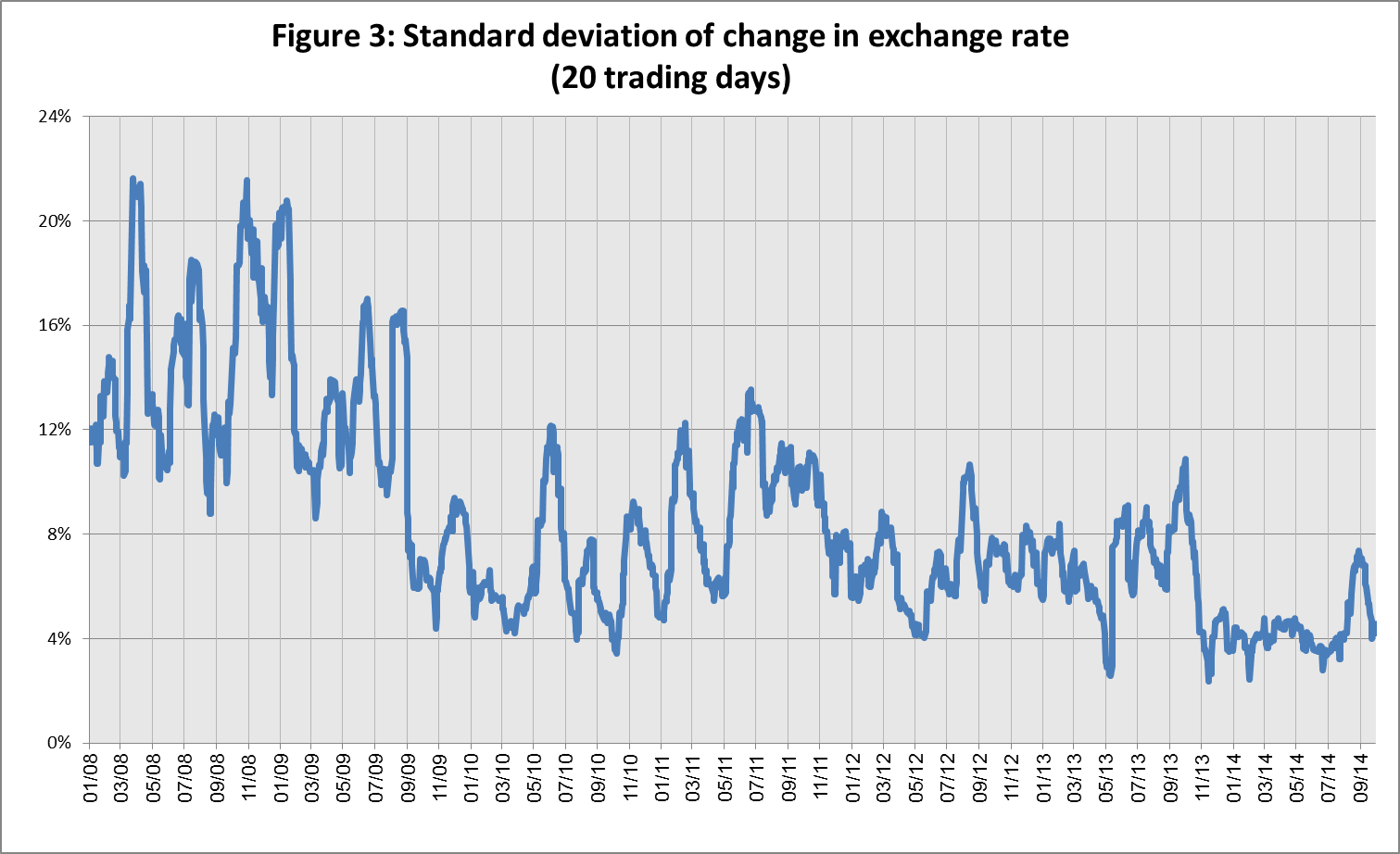

A decline in actual volatility of the exchange rate, in parallel with an increase in the implied volatility of the exchange rate.

The standard deviation of changes in the shekel-dollar exchange rate, which represents its actual volatility, declined in September by about 3 percentage points, returning to its average level of recent months, and was 4.3 percent at the end of the month.

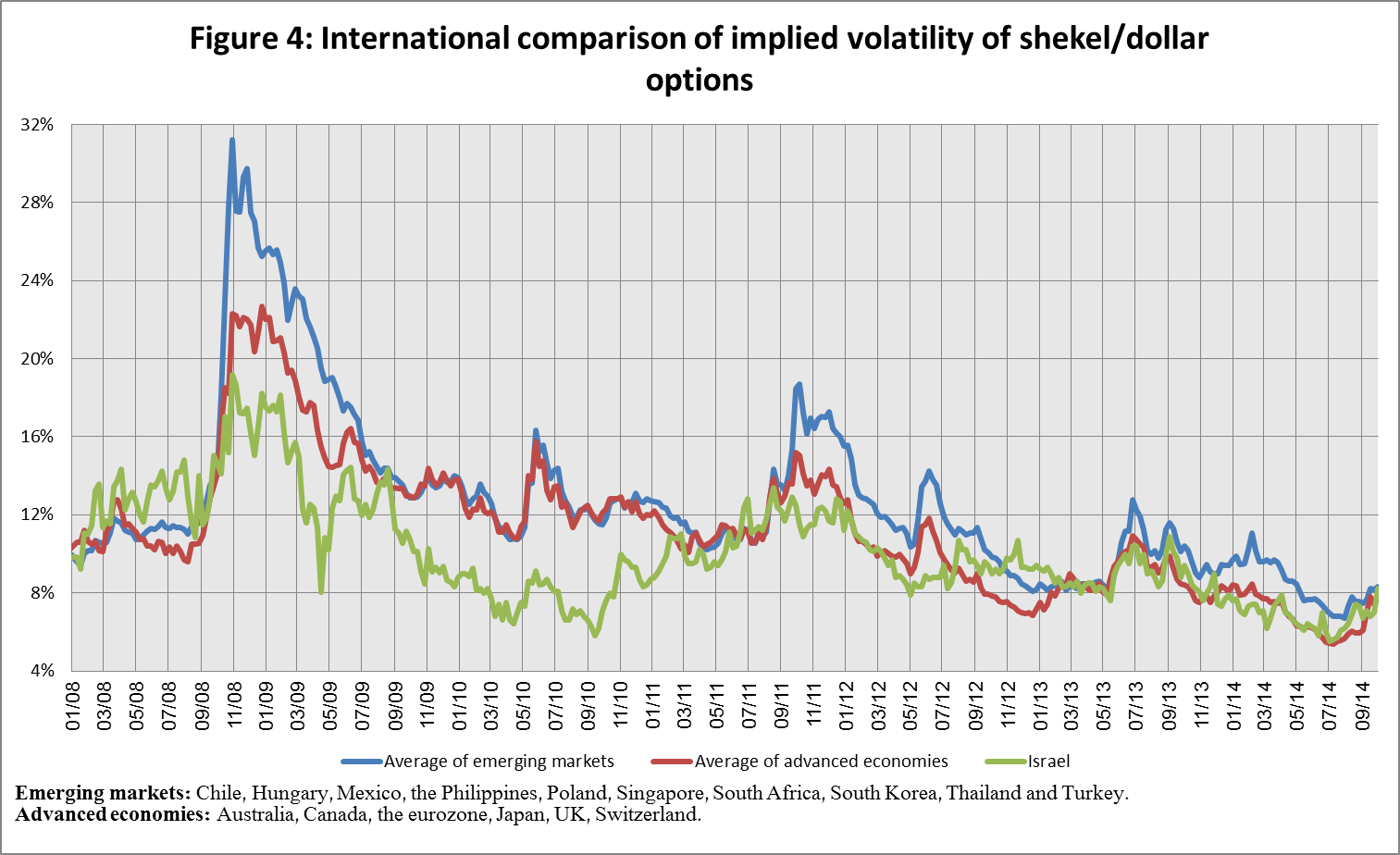

The average level of implied volatility in over the counter shekel-dollar options––an indication of expected exchange rate volatility––increased moderately, to 7.2 percent at the end of September, compared with 7 percent in August.

At the same time, in September, the implied volatility in foreign exchange options in emerging markets also increased, to 8 percent on average. The implied volatility in foreign exchange options in advanced economies increased as well in September, to 7.2 percent at the end of the month (see Figure 4).

3. The Volume of Trade in the Foreign Currency Market

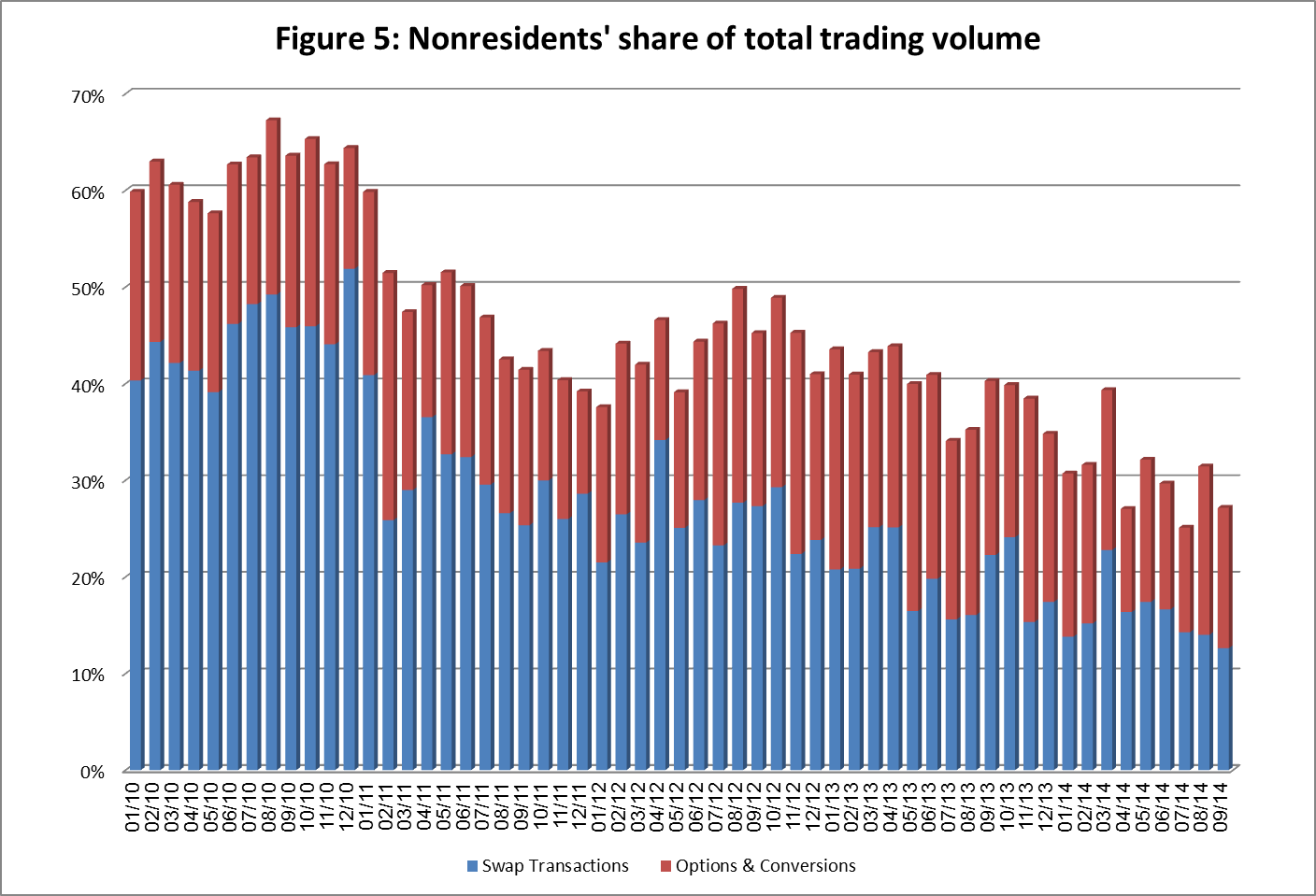

Total trading volume declined, as did nonresidents’ share of trading volume.

The total volume of trade in foreign currency in September was about $151 billion, compared with about $162 billion in August. Average daily trading volume declined by about 2 percent in September, to about $8 billion.

The volume of trade in spot and forward transactions (conversions) was about $45 billion in September. The average daily trading volume in those transactions increased in September by about 7 percent compared with August.

The volume of trade in over the counter foreign currency options totaled about $13 billion in September. The average daily trading volume in those options was about $680 million in September, a decline of about 20 percent compared with August.

The trading volume of swap transactions was about $92 billion in September, compared with $100 billion in August. Average daily turnover declined by about 3 percent from the previous month, to around $4.8 billion.

Nonresidents' share of total trade (spot and forward transactions, options and swaps) declined in September, to about 27 percent, compared with about 31 percent in August (see Figure 5).

Forex transactions with domestic banks, by instruments and sectors

($ million)

Conversions (1) |

Swaps[1] (2) |

Cross Currency swap[2] (3) |

Options[3] (4) |

Total volume of trade (1)+(2)+(3)+(4) | ||

September

2014

(Not final) |

Total |

45,195 |

92,141 |

962 |

12,894 |

151,192 |

Daily average (19 days) |

2,379 |

4,850 |

51 |

679 |

7,957 | |

Nonresidents |

17,464 |

18,939 |

0 |

4,369 |

40,772 | |

of which Foreign financial institutions |

16,860 |

18,488 |

0 |

4,305 |

39,653 | |

Residents |

27,731 |

73,202 |

962 |

8,525 |

110,420 | |

of which Real sector |

8,449 |

5,192 |

467 |

4,302 |

18,410 | |

Financial sector |

5,739 |

40,965 |

180 |

2,526 |

49,410 | |

Institutions (incl. insurance companies) |

4,129 |

9,505 |

85 |

0 |

13,719 | |

Individuals and provident funds |

1,481 |

9,299 |

0 |

514 |

11,294 | |

The Bank of Israel |

0 |

0 |

0 |

0 |

0 | |

of which within the program to offset the gas effect |

0 |

0 |

0 |

0 |

0 | |

Other[4] |

3,861 |

21 |

0 |

222 |

4,104 | |

Domestic banks[5] |

4,072 |

8,220 |

230 |

961 |

13,483 | |

August

2014 |

Total |

44,491 |

100,392 |

210 |

17,072 |

162,165 |

Daily average (20 days) |

2,225 |

5,020 |

11 |

854 |

8,108 | |

Nonresidents |

20,049 |

22,657 |

70 |

8,179 |

50,955 | |

of which Foreign financial institutions |

19,322 |

21,801 |

70 |

8,064 |

49,257 | |

Residents |

24,442 |

77,735 |

140 |

8,893 |

111,210 | |

of which Real sector |

7,210 |

5,784 |

10 |

4,294 |

17,298 | |

Financial sector |

4,140 |

42,984 |

0 |

2,273 |

49,397 | |

Institutions (incl. insurance companies) |

4,308 |

7,297 |

0 |

215 |

11,820 | |

Individuals and provident funds |

1,113 |

11,069 |

0 |

620 |

12,802 | |

The Bank of Israel |

585 |

0 |

0 |

0 |

585 | |

of which within the program to offset the gas effect |

585 |

0 |

0 |

0 |

585 | |

Other4 |

3,155 |

55 |

0 |

227 |

3,437 | |

Domestic banks5 |

3,931 |

10,546 |

130 |

1,264 |

15,871 |

[1] Only one leg of the swap, i.e., the nominal value of the transaction (in accordance with the BIS definition)

[2] The exchanged founds through Cross Currency Swap transactions considered for the volume, as one leg only in cases where the two legs offset each other.

[4] Including other entities such as portfolio managers, nonprofit organizations, national institutions, and those not include elsewhere.