· A depreciation of the shekel has a positive effect on exports: A depreciation of 1 percent leads to an increase of 0.3–0.6 percent in exports with a lag of two years.

· These estimates of elasticity are somewhat higher than those found in the past, and the lag of the effect is longer.

· The exchange rate’s effect on exports is higher in the manufacturing industries, particularly those of mixed technological intensity, than in the services industries.

Since 2008, the Israeli economy has been exposed to a prolonged appreciation of the shekel. This box examines the connection between the real exchange rate and exports, particularly since the beginning of the 2008 financial crisis, and also examines what industries are particularly sensitive to changes in the exchange. This analysis will help evaluate the extent to which the appreciation has weakened exports, and to what extent it is expected to weaken them in the future.

The appreciation of the shekel lowers the profitability of exports, since some of the exporters’ expenses (such as wages) are denominated in shekels in the domestic market while their income is denominated in foreign exchange. Shrinking profitability may lead to a decline in supply, thus reducing the volume of exports, and may have a negative impact on employment. Moreover, if firms stop exporting due to temporary exchange rate shocks, they may have difficulty returning to the markets when the terms improve—due to the costs of leaving and entering markets—which would lead to long-term damage.

Studies conducted around the world in the past[1] concluded that a depreciation of the local currency has a positive impact on exports, but assessments regarding the intensity of that effect varied from study to study. Studies in Israel generally found that a depreciation (appreciation) of 1 percent expands (contracts) export volumes by about 0.2–0.3 percentage points.[2]

Identifying how the exchange rate affects exports is no simple task, since the changes in the two variables affect each other: A real depreciation has a positive effect on exports, while an increase in exports leads—for different reasons—to a real appreciation, since the increase in the current account surplus increases the supply of foreign exchange. If these two effects take place simultaneously, the correlation between the exchange rate and exports is undetermined. However, it is reasonable to assume that changes in the current account and in capital movements have a rapid effect on the foreign exchange market, while the exchange rate’s effect on the quantity of exports is mainly with a lag.[3]

This assumption is essential in identifying the causal connection between the real exchange rate and exports, and it forms the basis of the examination presented here. If it is not valid, biased coefficients will be obtained in the regression, and this is particularly the cast for the coefficient representing the exchange rate’s lagged effect on exports. Another assumption at the basis of the analysis is that, in addition to the observed variables controlled for in the equation, including world trade, there are no unobserved variables that affect both exports and the exchange rate in parallel. In this case as well, biased coefficients will be obtained in the regression if the assumption is not valid. In view of the possibility that our assumptions are not fully valid, we must be cautious in giving a causal interpretation to our findings concerning the link between the exchange rate and exports.

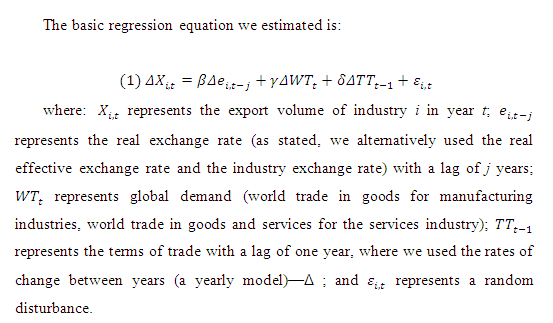

We estimated the elasticity of the export volume relative to the real exchange rate through regressions that use annual data from 1995 to 2015, while controlling for global demand (world trade) and the terms of trade (export prices divided by import prices)[4]—a variable that reflects the changes in the costs of imported raw materials, which affect the costs of production for export, and therefore also export supply. However, since a reverse effect—from exports to the terms of trade through export prices—is also possible, we used the terms of trade variable with a lag of one year.

In addition to the average elasticity in the economy, we also estimated the elasticity in six manufacturing industries that export most of their output (textiles, rubber and plastic, pharmaceuticals, electronics, chemicals, and machinery and equipment), and in the services industry (while distinguishing between business and tourism services). In order to examine the link between the exchange rate and the volume of exports (as opposed to its monetary value), we divided the industry export data by the export prices by industry.[5] We used two indices alternatively for the exchange rate: the real effective exchange rate (the ratio between the Consumer Price Index in Israel and the weighted average of the CPIs in the trading partners) and exchange rates adjusted for each industry (the industry export prices, translated into shekels, deflated by the general GDP deflator). While the exchange rates based on industry export prices better reflect the relevant price ratio for each industry, there are two problems inherent in them. First, the measurement of exports prices is of limited quality. In the manufacturing export price index, there is no proper control over the quality of the products, and the composition of products may also have an effect on it. In the services industries, there is a structural difficulty in distinguishing between quantity and price. Second, the industry price is also affected by technological changes and cost changes, which are expected to lower prices and thereby lower the industry exchange rate and increase the quantity exported (increase in supply). In other words, a negative correlation is created between exports and the industry exchange rate. In addition, since the security situation[6] has a very significant effect on tourism exports, we added a dummy variable for years in which the security situation worsened (1996, 2001, 2002, 2006, 2009, 2012, 2014).[7]

We estimated Equation (1) in two regression frameworks. The first includes a panel of eight industries, over a period of 19 years.[8] The weight of each industry in the regression is determined by its average weight in total exports analyzed here. The second framework includes specific equations for each industry following the SUR method[9], which takes into account the fact that the equations are dependent on each other.[10]

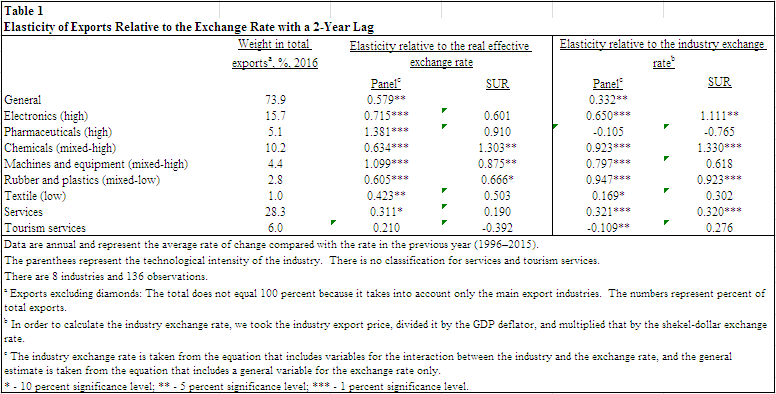

In estimating the equations, we included the changes in the real exchange rate with a lag of two years, assuming that the exchange rate does not affect exports within one year.[11] In estimating the first framework—the overall estimate of all industries included in the model excluding the unique elasticity of each industry—we found a positive and significant link between exports and the real exchange rate (both effective and industry) with a lag of two years: a depreciation of 1 percent increases the volume of exports by about 0.3–0.6 percent after two years (Table 1). Furthermore, a positive but insignificant connection was found with a lag of one year. The lag in the effect may be a result of the fact that agreements between exporters and foreign entities are based on long-term contracts, covering approximately two years in advance. Moreover, in this range, there are hedging transactions against the exchange rate.[12] We therefore focused on the exchange rate with a lag of two years. When conducting the examination through a variable for the interaction between the period following the global financial crisis (2009–2015) and the change in the industry exchange rate, we found that there is no significant change in the effect.

The unique link between the exchange rate (with a lag of two years) and exports of the various industries was estimated, as stated, through two regression frameworks: fixed effects based on panel data, and SUR. The results of the regressions are presented in Table 1, and show that in most industries, the exchange rate has a positive and significant effect on exports. The two estimation methods produce similar results in most industries. The results also show that the manufacturing industries, other than pharmaceuticals, are affected by the exchange rate more than the services and tourism industries. In the manufacturing industries, the average effect is about 0.8 percent, while in business services it is about 0.3 percent. In tourism—an industry that is very exposed to changes in the security situation—the coefficient is lower, and in most estimations it is not significant.[13]

Among the manufacturing industries, the mixed-technology industries are more affected by changes in the exchange rate, and their elasticity is close to one, similar to the findings in Bank of Israel (2009). The results in the pharmaceuticals industry vary in accordance with the exchange rates used in the examination: The real effective exchange rate produces a positive coefficient that is close to 1, while the industry exchange rate produces a negative and non-significant coefficient. This may be a result of technological changes that took place in the industry during the sample period, creating a negative correlation between the industry exchange rate and exports.

In order to examine the robustness of the results, we conducted a few examinations, with the findings remaining as they were[14]: The elasticity of exports relative to the exchange rate is positive, slightly higher than the results that were obtained in the past, reaching peak strength with a lag of two years. These findings are also true when examining each industry separately, and are particularly the case in mixed industries.

BIBLIOGRAPHY

(in Hebrew)

Lavi Y. and Y. Friedman (2007), “The Real Exchange Rate and Israel’s Foreign Trade”, Bank of Israel Review, 79, pp. 37–86.

Soffer, Y. (2005), “Measuring the Real Exchange Rate and its Influence on Exports and Imports”, Issues in Foreign Exchange, 1/05.

Sharabany, R. (2014), “The Effect of Terror, Image and Economic Variables on Various Types of Tourist Visits to Israel”, Discussion Paper 2014.05, Bank of Israel Research Department.

(in English)

Baldwin R. and P. Krugman (1989), "Persistent Trade Effects of Large Exchange Rate Shocks", The Quarterly Journal of Economics 104.4: 635–654.

Bank of Israel (2009), Annual Report for 2008, Box 2.3: “The factors determining manufacturing exports”.

Das S., M. J. Roberts and J. R. Tybout (2007), "Market Entry Costs, Producer Heterogeneity, and Export Dynamics", Econometrica 75.3: 837–873.

IMF (October 2015), World Economic Outlook.

Pradhan M., R. Balakrishnan, R. Baqir, G. Heenan, S. Nowak, C. Oner, and S. Panth (2011), "Policy Responses to Capital Flows in Emerging Markets", IMF staff discussion note, SDN/11/10.

[1] Baldwin and Krugman (1989); Das (2007); Pradhan (2011); IMF (2015); Leigh et al. (2017).

[2] Sofer (2005); Lavi and Friedman (2007); Bank of Israel (2009).

[3] A slight and temporary appreciation is not expected to have a significant effect on the quantity of exports, but mainly on profitability. But it is likely that a significant and prolonged effect on profitability will lead to a quantitative impact, and we will therefore observe a lagged effect.

[4] Due to data availability constrictions, we used the same data regarding global demand and terms of trade for all industries.

[5] For manufacturing, we used foreign trade data, and for services we used National Accounts data.

[6] See Sharabany (2014).

[7] We included the effect of the dummy variable only in the examination concerning the tourism industry.

[8] The regression assumes fixed effects for each of the industries, which fixes the marginal effect of each industry separately, thereby making it possible to distinguish the existing differences between industries in the average rate of increase of exports.

[9] Seemingly Unrelated Regressions.

[10] Furthermore, we added a dummy variable for one outlier export observation (in 2000, the electronic industry increased the quantity of exports by 70 percent). Excluding this dummy variable, higher elasticities are obtained relative to the exchange rate, particularly in the electronics industry.

[11] When estimating the overall export equation using the exchange rate with no lag, it obtains a negative and significant coefficient, which is consistent with the possibility that exports affect the exchange rate. We first estimated the equations using lags of one and two years, and then using only lags of two years.

[12] The appreciation survey conducted by the Industrialists Association for 2010 found that 81 percent of manufacturers make hedging transactions, and among the large exporters, the rate is even higher, at 93 percent.

[13] Sharabany (2014) found that the elasticity of exports relative to the real exchange rate is negatively dependent on the level of terrorism. It is 0.3 when there is a high level of terrorism, and close to 1 when the level of terrorism is low.

[14] Among other things, we estimated a sample that includes only the years 2003–2015; equations where we deleted one year each time; equations where we deleted certain industries each time; we used an interaction variable for the tourism industry with no lag; and we used the rate of change in the fourth quarter relative to the fourth quarter of the previous year.